Latin America wind energy market refers to the wind energy industry of Latin America‚ defined as the set of economic activities based on the consumption of wind energy through the development of wind farms to generate clean‚ renewable electricity in the countries of South America and Central America‚ through the use of advanced wind turbines in both onshore and offshore wind farms․ With ideal wind conditions in the northeast of Brazil and in Argentina’s Patagonia region‚ as well as ambitious national decarbonization targets‚ wind energy is one of the key drivers helping the region become a sustainable‚ climate-resilient energy market․

What Is the Current Size of the Latin America Wind Energy Market?

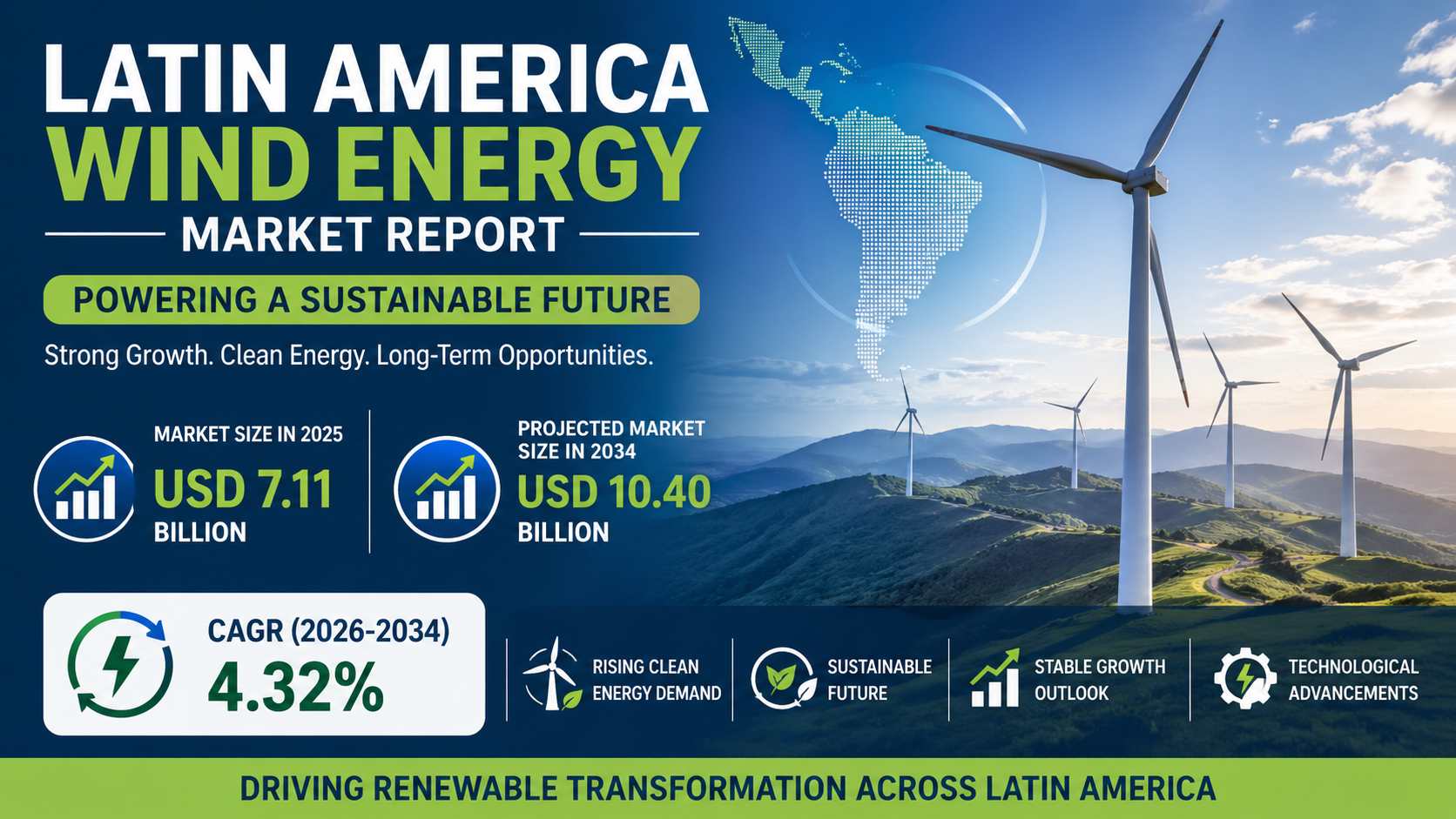

The Latin America wind energy market has become one of the largest players in the global renewable energy transition‚ the market is anticipated to be valued at USD 7․11 Billion by the year 2025- this figure shows the industry’s increasing success in integrating wind power into national grids․

According to the latest report by IMARC Group‚ titled ‘Indian Pharmaceutical Industry Growth Rate: the market is expected to reach USD 10․40 Billion by 2034 at a CAGR of 4․32% during the forecast period (2026-2034)․ This is attributed to government policies‚ huge investments on infrastructure‚ and increasing corporate demand for green energy by creating dedicated green procurement models․

Why is onshore deployment dominating the regional wind market?

Onshore wind is by far the leading technology in terms of installed capacity‚ with 86% of the total in 2025․ This is partly due to the relative maturity of land-based wind technology‚ but also to lower costs compared to newer offshore installations․

Several factors contribute to the strength of the onshore segment:

• Established Supply Chains: In countries like Brazil‚ supply chains such as manufacturing plants already exist to save lead time and costs․

• Enormous Land Availability: The wind-swept plains of the northeast of Brazil and mountainous valleys of Patagonia offer large areas for the construction of wind farms․

• Proven Reliability: With decades of technology history‚ onshore wind farms are more attractive to conservative institutional investors and development banks than offshore․

How Is Brazil Leading Latin America’s Wind Energy Market Share?

34% of the installed capacity is in Brazil‚ which takes first place in South America and fourth in the world‚ and the reasons are the wind potentials of the Brazilian northeast‚ especially in Bahia‚ Rio Grande do Norte and Piauí․

Brazil’s development has benefited from regulatory support (such as competitive energy auctions and specific tax exemption)․ In January 2025‚ President Luiz Inácio Lula da Silva passed a law creating the regulatory framework for offshore wind in Brazil‚ which was a decisive turning point for the start of the offshore wind industry․ With the creation of the law‚ Brazil has the necessary regulation and the incentives to make exploratory offshore wind farms in the territorial sea feasible and attract investments for the next frontier in clean energy․

What Are the Key Drivers Easing Wind Power’s Rapid Expansion in Latin America?

The Latin America wind energy market is driven by three factors:

• Supportive Government Policies: Chile‚ Colombia and Mexico all have set ambitious renewable energy targets and have provided the sort of support to project developers such as grid priority access and long term Power Purchase Agreements (PPAs)․

• Transmission: Considerable capital is spent to modernize transmission lines and to alleviate historic bottlenecks in the power grid to make it easier for wind power to reach population and industry centers․

• Corporate Decarbonization: Large industrial users‚ including mines and data centers‚ seek to contract directly with wind generators to achieve sustainability objectives and stabilize their costs of electricity․

How are technological innovations improving the efficiency of wind turbines?

The market is also benefiting from innovations in wind turbines․ Manufacturers are making larger turbine designs‚ usually in the 4 to 6 megawatt capacity range‚ along with taller tower heights and larger rotors to better harvest energy from variable wind speeds․

Modern technological trends include:

• Advanced Materials: The lightweight composite of the blades increases durability and their aerodynamic efficiency․

• Digital integration: With the use of Artificial Intelligence (AI) and predictive maintenance systems‚ operators can monitor their performance in real-time‚ reducing downtime and long-term operational costs․

• Smart Grid Solutions: Improved integration technologies ensure variable wind power can smoothly be fed into national grids without jeopardizing power stability․

What is the role of corporate PPAs in reaching market maturity?

A corporate PPA is another major restructuring of the market․ In liberalized markets like Brazil and Chile‚ industrial customers no longer rely solely on utility power purchases but are signing corporate PPAs directly․ Instead‚ they typically enter into long-term bilateral contracts with the wind farm developers․

In January 2025‚ the São Paulo Metro signed a fifteen-year contract to self-generate wind and solar power from a wind solar complex in Piauí․ In April 2024‚ ArcelorMittal and Casa dos Ventos signed a joint venture agreement for a large wind power project in Bahia․ They provide revenue certainty to project developers and lower financing costs‚ speeding up the construction of new generation capacity․

What Are the Main Barriers to the Latin America and Caribbean Wind Energy Market?

The industry nevertheless faces a number of challenges that could limit its growth:

• Transmission Bottlenecks: A large fraction of the highest quality wind resource is far from load centers with unmet demand‚ and lack of transmission to evacuation points can cause wind projects to be curtailed and investments to become “stranded assets”․

• Environmental and social impacts: Since wind farm development often faces resistance or requires community consultations and environmental impact assessments‚ there can be challenges if indigenous people use the land or if sensitive wildlife populations are present․

• Financial Volatility: Hefty upfront capital costs and currency volatility in some Latin American countries may heighten risk and impact returns for foreign investors․

Sample Request For Your Business

Which Other Countries Are Emerging as Meaningful Vaping Wind Power Hubs?

While Brazil leads‚ other countries have begun to diversify their energy matrix as well․

• Chile: The Atacama Desert has high winds․ The Chilean electricity market has been liberalized․ As of September 2025‚ Chile’s largest operating wind farm is Colbún’s Horizonte‚ with 140 turbines‚ in the Atacama region․

• Argentina: The economy faces many hurdles‚ but the Patagonia region has some of the world’s highest capacity factors and attracts interest․

Colombia and Peru: Both countries have yet to catch up with the regional leaders with growing focus on regulations to develop opportunities for both onshore and future offshore activity․

Conclusion:

The Latin America wind power market is at a turning point where wind power will go from a complementary source of power generation to being one of the most important sectors of the regional economy․ It is expected to reach USD 10․40 Billion by 2034‚ with technology and policy overcoming its current barriers․ With Brazil opening up for offshore developments and corporate energy procurement becoming the major driver‚ wind power will continue its vital role in Latin America’s energy security and green energy transition․